[ad_1]

da-kuk/iStock through Getty Photographs

The COVID-19 pandemic retains the power to throw the Vietnamese manufacturing sector astray in 2022 regardless of an absence of virus containment measures, primarily via the impression of workers shortages as contaminated employees are unable to contribute to manufacturing. This was actually the case in March as the most important wave of the pandemic thus far peaked in Vietnam and lots of employees have been compelled to remain at dwelling.

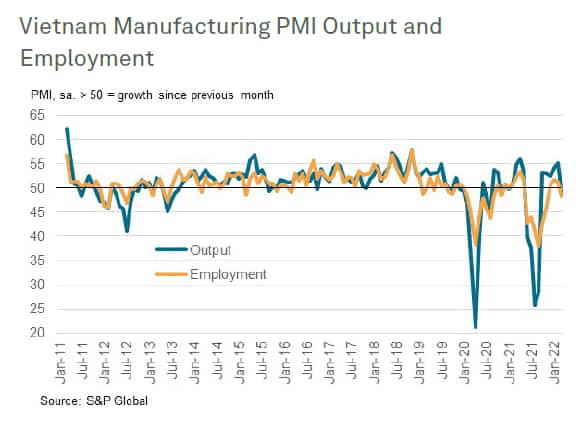

The S&P World Vietnam Manufacturing PMI signalled a fall in output for the primary time in six months on the finish of the primary quarter, stalling the restoration from final 12 months’s Delta wave. Companies primarily linked the drop in manufacturing to the impacts of the pandemic, with widespread infections amongst workers which means that they have been unable to work, thus limiting companies’ productive capability. Nevertheless, thus far, the downturn ensuing from the Omicron wave has not been as extreme as prior waves of the virus.

S&P World

Up till March, companies had been in a position to proceed to increase manufacturing regardless of the unfold of the virus because the authorities in Vietnam moved away from the ‘zero-COVID’ coverage, carried out within the first a part of the pandemic, to 1 that’s extra in step with dwelling with the virus and avoiding restrictions on financial exercise. The sheer quantity of infections within the newest Omicron wave, nonetheless, led to disruption regardless of a relative lack of restrictions.

That stated, the absence of lockdowns and non permanent firm closures this time round signifies that output declined at a a lot softer tempo than within the earlier wave.

Infections result in decrease workers numbers

In fact, staffing capability has been an issue for Vietnamese producers for the reason that Delta wave of the pandemic in the midst of final 12 months. Throughout that wave, individuals escaped bigger cities and COVID-19 hotspots to return to their hometowns. Ongoing considerations across the pandemic meant that they have been gradual to return to city areas, one thing respondents to the PMI survey talked about often in direction of the top of 2021 as having restricted workforce numbers.

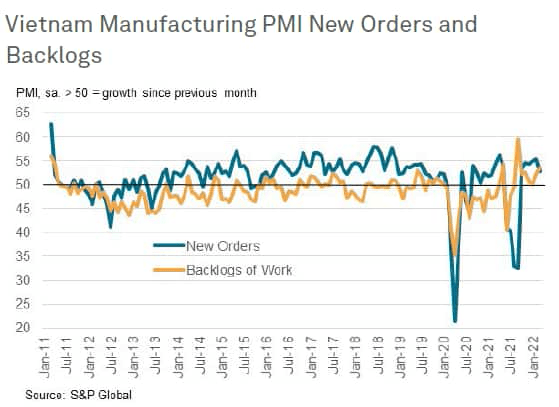

Employment continued to fall sharply via to final November, even after a stable restoration in workloads had been recorded, and rose solely barely within the three months to February. In consequence, producers have been unable to maintain up with workloads, seeing backlogs of uncompleted orders enhance in six of the previous seven months, and to a report extent final September. There had been hopes that extra employees would return following the Tet pageant in February, however the virulence of the Omicron variant put paid to this.

Writer Writer

Worth pressures mount

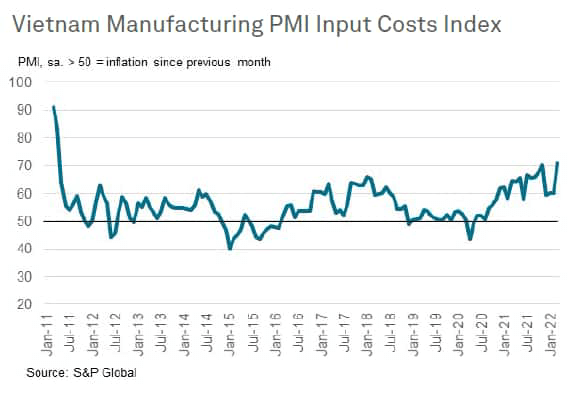

In addition to the disruption brought on by the pandemic, companies additionally confronted extra intense inflationary pressures in March. Enter prices rose on the quickest tempo in virtually 11 years amid reviews of upper costs for oil and gasoline particularly because the warfare in Ukraine prompted costs to surge. Output expenses additionally elevated at a a lot quicker tempo accordingly. A spell of elevated inflation might act to choke off demand, additional limiting total sector progress.

Writer

An infection charges easing

On a extra constructive word, the present wave seems to have peaked in mid-March, with an infection charges easing in direction of the top of the month. This could hopefully imply that extra employees can return to factories, boosting working capability through the second quarter and enabling companies to work via backlogs. S&P World nonetheless anticipates GDP to rise 5.8% in 2022 because the financial system recovers from the Delta wave in 2021, however the newest PMI knowledge illustrate that the pandemic nonetheless has the power to trigger issues within the financial system.

Authentic Submit

Editor’s Observe: The abstract bullets for this text have been chosen by Searching for Alpha editors.

[ad_2]

Source link

{kind=link}